This is a good companion guide to the question, “What type of life insurance do I need?” The reason is that once you decide you should buy life insurance, there are still lots of questions to answer. The two most important are the two listed above. In my opinion, the question on this page is #1 because, at the end of the day, you want to make sure you have the right AMOUNT of life insurance if something happens to you. Which type you had won’t matter because the death benefit pays the same way. However, if you have the correct TYPE for your situation, but not enough death benefit, then your beneficiaries are stuck with the consequences of incomplete planning.

There are numerous reasons to buy life insurance. The most common reasons include: to provide for surviving family members, to pay for a funeral, to pay off a debt, to support a small business you own and operate, to support a worthy cause, to leave a gift, etc. On this page, I am going to assume you are buying life insurance to provide for your surviving family members. Therefore, everything I say is geared towards that purpose. If you are buying insurance for a different reason, this page will not provide what you need. Now, I do include snippets about paying things off with life insurance, but that is only due to the nature of this article.

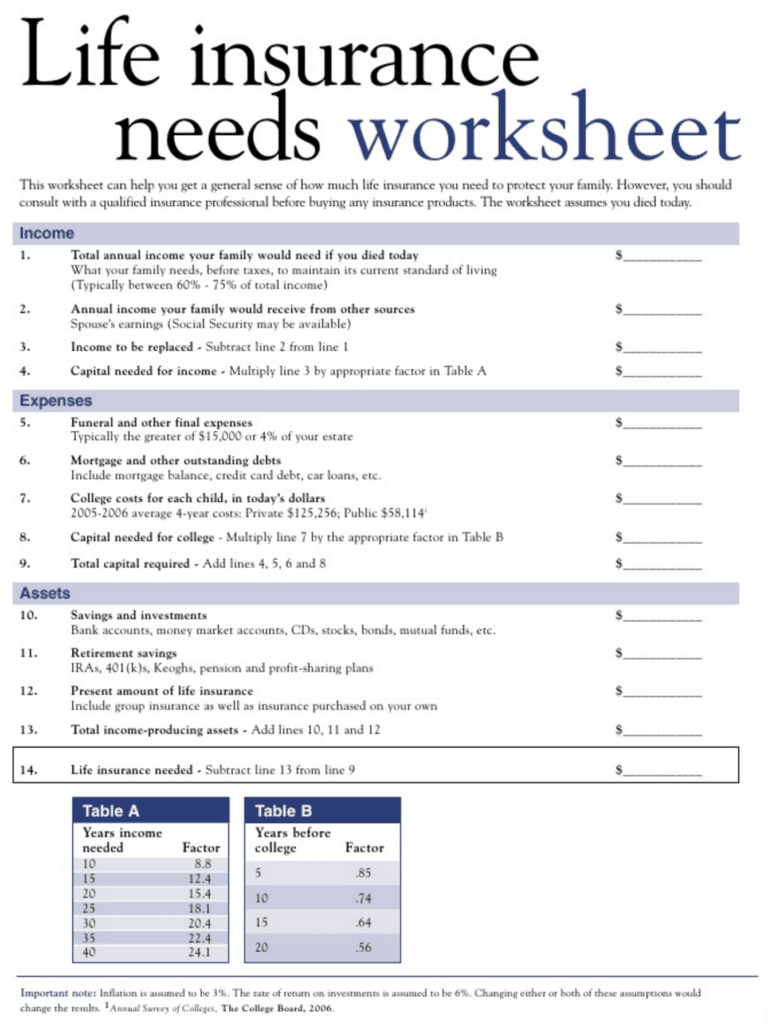

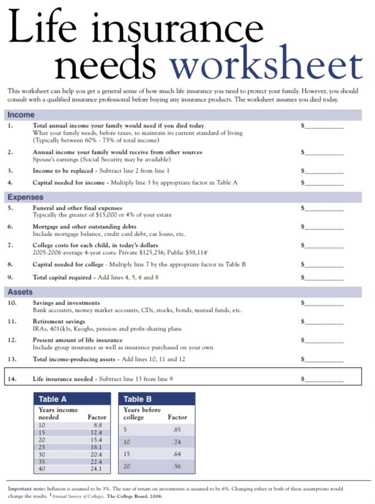

There are a couple of different ways to figure out how much life insurance you need. Most insurance companies have a standard “fact finder” that is designed to help applicants determine what amount of life insurance is appropriate. We’ll call this the “lump sum method.” I’ve included a sample below. This approach is good because it gets you thinking about almost everything that you could need money for in the event of a death. The basic formula goes like this:

(everything you owe money on) + (anything you might spend money on) + (lump sum as a buffer for income and/or misc. expenses) = (your life insurance number)

Sample fact finder here-------->

“The Quest stands upon the edge of a knife. Stray but a little, and it will fail, to the ruin of all. Yet hope remains while the life insurance is true.”

How much life insurance do I need?

Let’s break this down. For everything you owe money on, look at the picture above. The common items include: mortgage, auto loans, credit cards, student loans, & any other loans. You add all these things together and arrive at a number that will pay off all your debts. The obvious advantage to this is that your surviving family no longer has that monthly expense or the fear of having it repossessed by the bank. One of the sad outcomes of improper planning is the need for the surviving spouse to sell the house just to make ends meet. The car(only mode of transportation) could also be repossessed and then they have no way to get to school or work. If you want to give your survivors the best sporting chance, have enough insurance to pay these things off.

What about anything you might spend money on? The above picture has samples of those things too. They include, but are not limited to: groceries, medical expenses, school(including k-12 and college), utilities, gasoline, clothes, funeral expenses, insurance, etc. The way to look at this category is: what types of expenses do I normally have that I can’t pay off like a debt? What is a monthly recurring expense? If you have children, this category is always changing(usually getting more expensive). Kids outgrow clothes, tend to eat more as teenagers, begin driving(think car payment and car insurance costs), do more social activities, and various other things. This category can be much harder to estimate than your debts, but there are tools to help you figure this out. One note I’ll add here is if you intend to pay for college with life insurance, the total need goes WAY up. The increase is easily $250,000 per child to fully fund college and all other college expenses. If college isn’t in your gameplan, your number is much less in comparison.

Another note here is that everything is more expensive than you think it is going to be. What I always did for my clients was round up. So, if you follow the calculator or insurance form and arrive at a number like $324,560, then I would round up to $350,000 or $400,000. Some companies offer a price break at certain insurance amounts, meaning the cost per $1,000 of insurance coverage will be less if you purchase $500,000 instead of $400,000. I’ve seen cases where the insurance bill was actually LESS for $1,000,000 in coverage than it was for $800,000. That’s a no-brainer to take the higher coverage.

The last part of this formula is the lump sum. This part can answer two questions. First, how much of your income do you want to have available to your spouse? Second, do you want to throw in some extra coverage “just in case?”

The first question goes like this: if you make $50,000/year and your spouse relies on that income, do you want to keep it going for a certain period of time? For example, if you added an extra $300,000 of coverage after your fact finding, that would provide your spouse with 6 years of income replacement*. I’ll touch further on this point in a moment.

The second question covers the “you don’t know what you don’t know” fear. What are the chances that you’ll have everything planned out to the letter, but something unexpected will happen? That’s about as close to a 100% guarantee as you’ll ever have. Somebody will need surgery; some major repair need will arise; something crazy will happen that you couldn’t possibly expect. With an additional lump sum, you take the stress of this away, at least financially. I am always a fan of throwing in some extra if it’s in the budget. Emergencies have a way of happening when you don’t want them to. When you’re prepared, they tend to happen less.

The major drawback to this entire plan is that the money will run out eventually. Additionally, it can also be incredibly overwhelming to most people to consider every possible thing that could happen that costs money. Many clients would glaze over after a while, throw their hands up, and say “Just add X to it and let’s be done!” Fact finders are very comprehensive, but very overwhelming. If you have the patience for it and/or are a very detailed person, this should go well for you in the planning stage.

Every paragraph from my initial formula to now has related to the “fact finder” or “lump sum” method of determining how much life insurance you need. Now, I’ll discuss the other method. It’s called “income replacement method.” In contrast to the lump sum method, this method simply tries to replace your income. For example, let’s say you make $50,000/yr and you want your surviving spouse to still receive that income if you die. The first method would say, “How many years do you want this to last?” and you would multiply the years and the income. A $1,000,000 lump sum would last 20 years based on the simple math. It’s simple, but there is a glaring problem: the lump sum is going to run out eventually. What if it runs out too soon? What then? The answer is income replacement.

Instead of gradually depleting a lump sum, this method calculates how much of a lump sum investment would generate enough interest income to equal your income. For example, if you bought an investment for $1,000,000 that paid 5% annually, that would equal $50,000. The lump sum is never depleted, and the income arrives indefinitely. Theoretically, the surviving spouse could pass away and leave that lump sum interest income to a beneficiary, who would then enjoy it during their lifetime.

This method has three drawbacks. The first is that the insurance need is usually much higher. That means if you needed $1,000,000 in coverage on plan 1, you may need $2,000,000 for plan 2. If your death benefit is higher, that means your premium is higher too. The other drawback is the interest income isn’t guaranteed in most cases. You could have a really good year followed by a really bad year, and then your lump sum investment fell below your initial start. If that happens, you’ll need a greater return the following year to equal the income you need. The third problem is that it doesn’t account for inflation. $50,000/yr may be great now, but what about 10-20 years from now? What if we have another period like 2021-2023 where inflation skyrocketed? The ups and downs of the market and world events can affect your income negatively.

I mentioned above that the income isn’t guaranteed in most cases. The case where it is guaranteed depends on what your investment is. If your surviving spouse purchases a fixed annuity or another fixed product, then there is a guarantee. Interest guarantees are always lower than the positive potential earnings of non-guaranteed products. You won’t lose anything, but you also will need much more insurance to bank on your annual income requirement. This is something to talk to your insurance agent about to make sure you understand the risks. Make sure the agent has knowledge of these things. Many insurance agents are only out to sell as many policies as possible and don’t want to know this level of detail or don’t have the capacity to.

I know this article is longer than most, but I like to be thorough on important topics like this. At the end of the day, your death benefit need should be your top priority when picking out your life insurance. The type of insurance is the second consideration. Decide which of the two discussed methods makes sense to you, talk to your insurance agent, and get that insurance in place. We are never promised tomorrow. If you have a family and have zero life insurance in place--take action now!

*Most studies suggest that even if one of the parents dies, the total household monthly expense will still be 70-80% of what it was while that person was alive. It isn’t reduced by 50%. Yes, there is less food, less gasoline, less clothing, etc. but the monthly need is still more than most people think.

*from lifeinsuranceblog.net