Most of you reading this are probably paid every 2 weeks, likely on Fridays. If this applies to you, I am willing to bet that you’ve heard advice that sounds something like this: “Hey, you normally get 2 paychecks a month, but for 2 months of the year, you get 3 paychecks. When that happens, put all that 3rd paycheck into a savings account for a rainy day. You’ll be glad you did.” While this advice sounds good, is it really an “extra” paycheck? How does it really play out? I’ll answer that question here. Read on!

On the surface, this all sounds true. You think, “I normally get 2 paychecks each month. This month I get 3 paychecks. Next month I’m back to 2. So, doesn’t that mean I get an extra check this month that I won’t need?”

Take a look at this simple budget:

Bills to pay each month from 1st-15th: House, Car, credit card, groceries, gas, misc. Total budget need is $2000

Bills to pay each month from 16th-31st: Insurance, utilities, subscriptions, groceries, gas, misc. Total budget need is $1800.

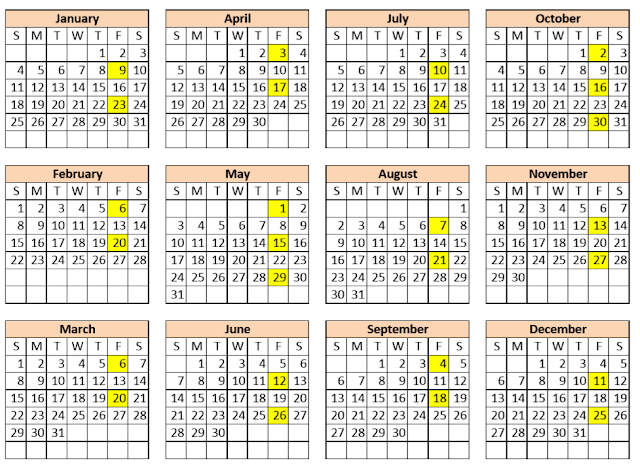

Now, let’s look at a paycheck calendar to help me illustrate the points I’m about to make:

*Courtesy of callcenterfocus.com

Let’s assume you get paid $2100 each paycheck. Your total monthly budget requirement is $3800. So, this leaves you with a net gain of $400 most months(If you want to get overly technical, you could say you get a total income of $4550/month. You do this by dividing the dollar total of all your paychecks for the year($54,600) by the number of months(12) in the year). Again, I’m going to use the $4200/mo number because that’s what you take home 10 months out of the year, and it’s what you would actually budget with.

In a real-life budget, you would have bills due throughout the month. I am saying in my example that we pay our first set of bills by the 15th and our second set by the last day of the month. If I added multiple payment due days, this would get overly complicated, and I’m trying to keep it simple.

Using the image above, let’s start in January. You get paid on the 9th. This is right in the middle of your first set of bills, so we’ll assume you used part of your last December check and part of your first January check to cover this set of bills. The same could be said as we move forward each paycheck until we get to May 1st. Keep in mind, each paycheck that you receive is going towards bills that are still coming due, so you’re saving $400/month at the most. In reality, you’re probably finding something to spend this on, so very little is actually being saved. Now, your last check in April covered the 2nd set of April’s bills. Now, you got paid on May 1st. What happens to this paycheck? You use it to cover the bills for the first half of May. You got all those bills paid and now you get your May 15th check. Is this the check you get to save? Nope, because you still have bills due from the 16th-31st of the month, remember? Your May 15th check has to go towards those bills. Ok, now you get paid on May 29th and life is good because you get to save it all since all of May’s bills are paid, right? Wrong again! The May 29th check must go towards the bills due the first half of June. Well dang, doesn’t that mean your June 12th paycheck gets to be saved? Nope! That goes towards the 2nd set of bills for June. On and on we go…

The point I’m trying to make here is that your bills will keep coming due the same time every month, regardless of when you get paid in the month. So, whether you get paid on the 9th and 25th, or get paid the 1st, 15th, and 29th, your check is still going towards bills because they are still coming due! You also still have to eat, still have to drive, still need other products, etc. Those needs don’t disappear 2 times a year. You might ask, “Wait a minute! If I normally get $4200 a month but then bring home $6300 in May, how am I not ahead by $2100!?” Well, when you assume your income is $4200/month and your expenses are $3800/month, the previous logic follows. However, that logic is deceptive because your number of $4200/month is based on 28 days(2 bi-weekly checks), but only one month a year ends after 28 days. The rest end on day 30 or 31. So, what happens with those 2-3 extra days each month? Do you discard those days completely in your calculation? No way! You are still getting paid for those days(at least in your salary calculations you are). So, in reality, you have to use the previous number of $4550/month that I mentioned above. Why? Because that’s based on your annual salary, which is a more accurate depiction of your true income. The $4550 salary number takes those extra 2-3 days per month into account, even though you feel like you bring home $4200/month based on when you receive your paychecks. That’s why you feel like your 2 months a year with triple paychecks is all extra money, because you’ve been thinking your monthly income is $4200 instead of $4550.

Here's another way to think about this. Suppose you were paid bi-monthly on the 1st and 15th each month, and each check was $2100. That means you get 24 paychecks every year, and you consistently get paid on the 1st and 15th every month. Your annual salary is: $2100 x 24 = $50,400. Remember, this number is less than the previous example because we are using 24 paychecks per year instead of 26. Now, if you had 2 months a year in this scenario where you were paid on the 1st, 15th, and 25th, would that be an extra paycheck? YES! The reason is because your true monthly income is already calculated as $4200/month. ALL days per month are factored in. There aren’t 2-3 extra days per month to consider here. Therefore, your true monthly income is $4200 and your monthly expenses are $3800, making your net gain at the end of each month $400. If you had a month where you pop an extra paycheck of $2100 on top of that, then that full check would go directly towards the “extra” category. Your expenses are already covered by your normal 2 checks, leaving you with an entire extra paycheck, or playcheck, to work with. Make sense?

So, does this mean your “extra” paycheck from the bi-weekly system just magically vanishes because of those pesky bills and you’ll never get to save? By no means! It’s just a bit harder to anticipate. What I mean is that your mortgage may be due on the 1st of the month, your car on the 8th, your insurance on the 12th, etc. You will have rotations in your paychecks where you have already used “Paycheck 1” to cover your upcoming mortgage, but then you coincidentally receive “Paycheck 2” the day before your mortgage is due. If the timing falls like this, it may feel like you have extra money because you covered your mortgage with 1 check in advance. This feeling doesn’t happen because of “extra” funds, but because of the timing of your bills vs. paychecks. Again, your true monthly income is set at $4550 when averaged out for the year. But you can’t set a monthly budget with that number because you bring home $4200 for 10 months our of the year.

If this still seems confusing, I get it. I consider myself a fairly intelligent person, and I didn’t pick up on this until I was already in finance for several years. In fact, I used to give seminars to business and schools where I took a compliance-approved powerpoint presentation and told the entire audience to save that “extra” paycheck each month when they got 3 checks instead of 2! That advice was on one of the slides and in my presenter notes. I was teaching this myth and so was everyone else in my organization that was using the same presentation!

What opened my eyes to this was when I worked at one bank where we were being paid bi-monthly for a long time, but then suddenly switched to bi-weekly. When that happened, my paycheck amount was LESS each time, and I panicked. I had been budgeting based on my bi-monthly paycheck system, and it allowed me to stay consistent from month to month. When we switched to bi-weekly, it all fell apart, because my income for 10 months out of the year was considerably less than I had been accustomed to bringing home. However, my annual income amount was the same; it was just delivered to me differently, which messed up my budget.

It’s just like having two people run the same race. Person A starts running at the same speed during the entire course of the race. He never speeds up or slows down. Person B starts the race at a slower pace. However, at 2 points during the race, his adrenaline kicks in and he speeds up for a time, but then slows back down to the slower pace. Both people finish the race at the exact same time. Person A is like the bi-monthly system. Person B is like the bi-weekly system. The finishing result is the same. The audience could watch the race and think that Person B was going to lose for most of the race. Much to their surprise, the runners finish at a tie.

So, what do you do with this information? Honestly, probably nothing. If you’ve already been budgeting and spending with the habit of bi-weekly paychecks, then you don’t change anything. The only thing that really changes is the knowledge you have about those special 2 months of the year. Now, you can go forward knowing it really isn’t those 2 months where you save extra; it’s truly during the year where you pick the “extra” from random points and it adds up at the end of the year. Also, you know why you’ve been going for years thinking, “Hey! I thought this was my extra paycheck month! Where did it all go!?”

Now you know.

The "Extra" Paycheck